June 5, 2026

Apartment NOI: The Metric That Drives Multifamily Value

Unlock the value of your multifamily investments with apartment NOI. Learn how to calculate this key metric and avoid costly mistakes!

Apartment NOI, the industry-standard term for net operating income, is defined as a multifamily property’s total revenue minus all operating expenses, excluding debt service, income taxes, capital expenditures, and depreciation. It is the single most important number in multifamily investment analysis because it measures a property’s intrinsic earning power independent of how it is financed. Investors use apartment NOI to calculate cap rates, qualify for loans through the Debt Service Coverage Ratio (DSCR), and compare properties across markets. Understanding how to calculate it accurately, and where analysts routinely go wrong, separates disciplined underwriting from costly mistakes.

What is apartment NOI and how do you calculate it?

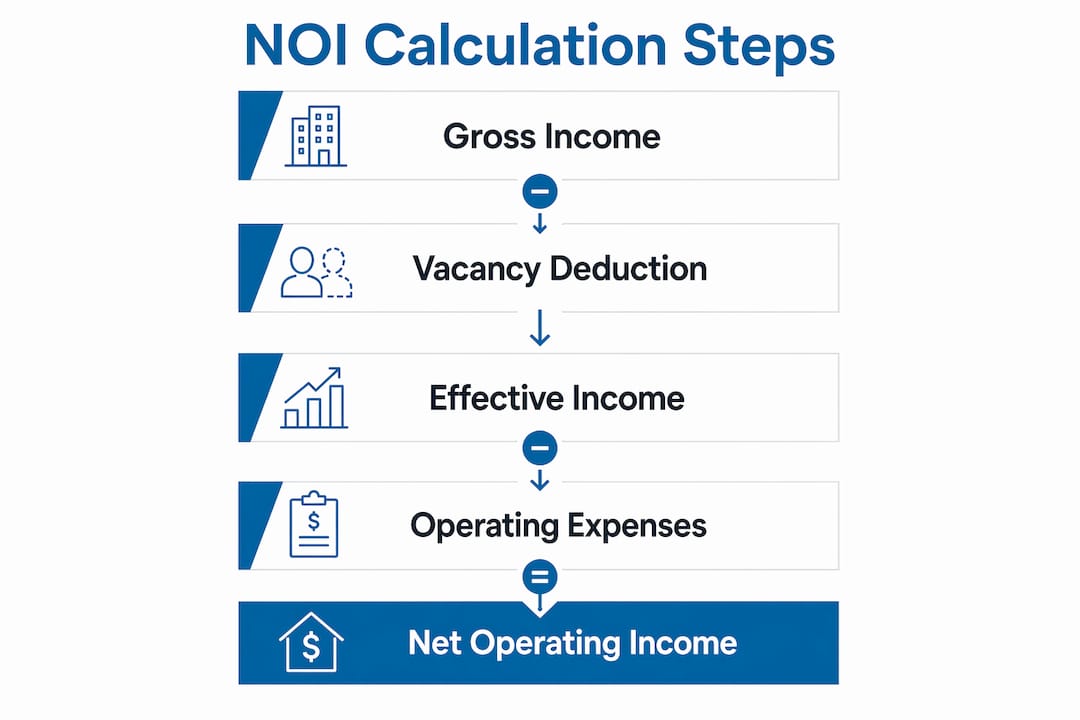

NOI calculation follows a straightforward sequence, but each step contains decisions that can materially change the result. The formula is: NOI = Effective Gross Income (EGI) minus Total Operating Expenses.

Step 1: Build gross potential income (GPI)

GPI is the maximum revenue a property could generate if every unit were occupied at market rent for the full year. For a 50-unit building averaging $1,800 per month per unit, GPI equals $1,080,000 annually. This is your ceiling before any adjustments.

Step 2: Deduct vacancy and credit loss

Vacancy and credit loss deductions are the standard bridge from GPI to effective gross income. Vacancy accounts for physically empty units; credit loss covers tenants who occupy units but do not pay. A 5% combined deduction on the example above yields an EGI of $1,026,000.

Step 3: Add ancillary income

Multifamily properties generate revenue beyond base rent. Common ancillary income sources include:

- Parking fees and garage rentals

- Pet fees and pet rent

- Laundry and vending machine income

- Storage unit rentals

- Package locker access fees

- Late fees and lease termination fees

Adding $30,000 in ancillary income brings total EGI to $1,056,000.

Step 4: Subtract operating expenses

Operating expenses in multifamily NOI calculations include property taxes, insurance, repairs and maintenance, common-area utilities, property management fees, and administrative and marketing costs. For the example property, assume total operating expenses of $422,400, which represents a 40% expense ratio. That is squarely within the typical stabilized range.

NOI = $1,056,000 minus $422,400 = $633,600

What is explicitly excluded: mortgage principal and interest, capital expenditures such as roof replacements or HVAC upgrades, income taxes, and depreciation. NOI excludes financing and tax costs specifically to allow consistent property comparison regardless of capital structure. Two identical buildings with different loan terms will show the same NOI, which is the point.

Pro Tip: The most common income-side error is treating gross scheduled rent as effective gross income without applying a vacancy factor. Even a 95% occupied property should carry a 5% vacancy and credit loss assumption. Omitting it inflates NOI and, by extension, inflates your valuation.

Why apartment NOI matters for valuation and underwriting

NOI is not just an income statement line. It is the engine behind two calculations that govern every acquisition and refinancing decision in multifamily real estate.

The cap rate relationship

The cap rate formula states: Property Value = NOI ÷ Cap Rate. This means NOI growth directly and mechanically increases property value. If the example property above trades at a 5.5% cap rate, its value is $633,600 ÷ 0.055 = approximately $11.52 million. Increase NOI by $50,000 through rent increases or expense cuts, and the same cap rate produces a value of $11.43 million… wait, $683,600 ÷ 0.055 = $12.43 million. That is nearly $910,000 in equity created from a $50,000 NOI improvement. This leverage effect is why sophisticated investors obsess over every line item.

Selecting appropriate cap rates is fundamental, since the cap rate mediates the entire relationship between NOI and value. A 25-basis-point error in cap rate assumption on a $10 million property can shift value by $400,000 or more. Treat cap rates as core assumptions that require market validation, not defaults.

Debt service coverage ratio and loan qualification

Lenders require DSCR ratios typically above 1.20 to 1.25, meaning NOI must cover annual debt service by at least 20 to 25 percent. If annual debt service on the example property is $480,000, the DSCR is $633,600 ÷ $480,000 = 1.32, which clears most lender thresholds comfortably. Drop NOI by $100,000 due to higher vacancy or rising expenses, and DSCR falls to 1.11, likely triggering a loan rejection or a required equity infusion.

The 2026 market illustrates this risk concretely. Mid-America Apartment Communities projected a 0.75% same-store NOI decline driven by expense growth outpacing rent growth. For a REIT with billions in assets, that fraction of a percent translates to tens of millions in lost value and tighter debt coverage across the portfolio.

“NOI is the only number that tells you what a property actually earns, stripped of every financing decision and tax strategy. Everything else in multifamily underwriting is downstream of it.”

Common pitfalls in calculating accurate apartment NOI

Accurate NOI calculation is harder in practice than the formula suggests. These are the errors that most frequently distort results and mislead buyers, sellers, and lenders.

-

Misclassifying capital expenditures as operating expenses. Misclassifying capital expenditures as operating costs can materially inflate NOI and mislead lenders or buyers. A new roof is a capital expenditure, not a repair. Booking it as maintenance understates true operating expenses and overstates NOI.

-

Omitting vacancy and credit loss. Sellers and sponsors frequently present pro forma NOI at 100% occupancy or with unrealistically low vacancy assumptions. Even Class A properties in strong markets carry 3 to 5 percent vacancy. Ignoring this produces an NOI figure that no actual property will achieve.

-

Excluding replacement reserves. Replacement reserves for future capital outlays sit below the NOI line in accounting terms, but analysts who exclude them from their underwriting expense stack understate the true cost of ownership. A common benchmark is $200 to $400 per unit per year for stabilized properties.

-

Understating management fees. Self-managed properties often show no management fee in historical financials. Any acquisition underwriting must include a market-rate management fee, typically 4 to 8 percent of EGI, even if the buyer plans to self-manage. This reflects the true economic cost.

-

Ignoring ancillary income inconsistencies. Revenue from laundry, parking, and storage can be legitimate and growing. It can also be one-time or seasonal. Verify that ancillary income is recurring and contractual before including it at full value.

Stabilized multifamily operating expense ratios often run roughly 35 to 50 percent of EGI. This range is your first sanity check. If a seller’s pro forma shows a 28% expense ratio on a 1980s garden-style property, something is missing.

Pro Tip: Sponsors often present NOI in marketing teasers, but experienced analysts re-derive NOI from scratch, verifying every expense category and reserve inclusion independently. Never accept a seller’s NOI figure without rebuilding it line by line from raw rent rolls and actual invoices.

How to improve apartment NOI: strategies that actually work

NOI improvement is the core thesis behind most value-add multifamily acquisitions. The strategies below are ranked by reliability and speed of impact.

-

Raise rents to market. The fastest NOI lever is closing the gap between in-place rents and current market rents. A property with rents 10% below market on 50 units at $1,800 average is leaving $108,000 in annual NOI on the table. Lease-by-lease rent increases at renewal, combined with unit renovations that justify higher rents, are the primary mechanism.

-

Add or optimize ancillary income. Properties that do not charge for covered parking, storage, or pet rent in markets where competitors do are leaving revenue uncaptured. Adding a package management amenity, for example, can generate direct fee income while reducing staff time spent on deliveries, a dual NOI benefit.

-

Reduce operating expenses without cutting service quality. Insurance premiums are frequently negotiable at renewal, particularly for owners with multiple properties who can consolidate coverage. Utility expense reduction through LED retrofits, low-flow fixtures, and submetering can cut common-area costs by 15 to 25 percent in older properties.

-

Maintain high occupancy through leasing velocity. Operational drivers like lease renewal rates, delinquency, and maintenance efficiency affect vacancy and expenses and serve as leading indicators of future NOI changes. Tracking 30-day and 60-day lease expirations, and acting on them early, prevents the vacancy spikes that compress NOI.

-

Optimize management fees and vendor contracts. Property management fees, landscaping contracts, and pest control agreements are all negotiable, especially for owners with scale. Renegotiating a management fee from 7% to 5.5% of EGI on a $1 million EGI property saves $15,000 annually, which at a 5.5% cap rate adds $272,000 in property value.

-

Invest in renovations with realistic NOI expectations. Value-add renovations work when the rent premium exceeds the annualized cost of the improvement. A $6,000 unit renovation that commands $100 per month in additional rent generates a 20% cash-on-cash return on that capital, and the NOI increase compounds into significant valuation gains. Review the multifamily amenities checklist to identify which upgrades deliver the strongest resident demand and retention.

Key takeaways

Apartment NOI is the definitive measure of multifamily property performance, and every valuation, loan, and investment decision flows directly from its accuracy.

| Point | Details |

|---|---|

| NOI formula | Total revenue minus operating expenses, excluding debt service, taxes, and capital expenditures. |

| Valuation link | Property value equals NOI divided by cap rate; a $50,000 NOI gain at a 5.5% cap rate adds roughly $910,000 in value. |

| DSCR threshold | Lenders typically require NOI to cover annual debt service by 1.20 to 1.25 times minimum. |

| Top calculation error | Omitting vacancy and credit loss, or misclassifying capital expenditures as operating expenses, materially distorts NOI. |

| NOI improvement | Raising rents, adding ancillary income, and cutting controllable expenses are the three most reliable NOI levers. |

What experienced analysts know about apartment NOI that pro formas hide

At Locker Solutions, we work closely with property managers and multifamily operators across the country, and the pattern we see most often is not fraud. It is optimism. Sellers present pro forma NOI built on best-case occupancy, below-market expense assumptions, and ancillary income that has never actually been collected. Buyers, eager to win competitive deals, accept those numbers with insufficient scrutiny.

The discipline that separates strong performers from troubled acquisitions is simple: rebuild NOI from the rent roll up, not from the offering memorandum down. Verify every expense with actual invoices. Apply a market-rate management fee even if you plan to self-manage. Use a vacancy assumption grounded in the submarket’s trailing 12-month data, not the seller’s current occupancy on the day of marketing.

We have also observed that operators who track leading operational indicators, things like 60-day lease expiration exposure, maintenance response times, and package delivery complaint rates, consistently outperform those who only review NOI quarterly. NOI is a lagging metric. By the time it deteriorates, the operational problems causing it have been compounding for months. The investors who protect NOI are the ones watching the inputs, not just the output.

Conservative underwriting is not pessimism. It is the only way to build a margin of safety into a deal that will face unexpected expenses, market softness, or interest rate pressure at refinancing. The ROI of multifamily amenities follows the same logic: every capital decision should be stress-tested against a realistic NOI scenario, not a best-case one.

— Locker Solutions

How Locker Solutions supports multifamily NOI optimization

Property managers focused on NOI improvement need amenities that generate revenue, reduce staff workload, and retain residents without adding significant operating cost. Locker Solutions provides Luxer One® package lockers and automated package rooms purpose-built for multifamily properties. These systems reduce front-desk package handling time, cut resident complaints about missed deliveries, and can generate direct fee income as an ancillary revenue stream. For properties competing to attract residents in markets where the best apartments offer premium amenities, package management infrastructure is a measurable differentiator. Explore Locker Solutions’ full range of package lockers and rooms to see how they fit your property’s operational and NOI strategy.

FAQ

What does NOI mean for an apartment property?

NOI, or net operating income, is a multifamily property’s total revenue minus all operating expenses, excluding mortgage payments, income taxes, and capital expenditures. It measures the property’s income-generating ability independent of financing structure.

What expenses are excluded from apartment NOI?

Mortgage principal and interest, income taxes, depreciation, and capital expenditures such as roof replacements or major system upgrades are all excluded from NOI. These items are excluded because they vary by ownership structure and financing, not by property operations.

What is a good NOI for an apartment building?

There is no universal target, since NOI depends on property size, market, and asset class. The more useful benchmark is the expense ratio: stabilized multifamily properties typically run operating expenses at 35 to 50 percent of effective gross income, implying NOI margins of 50 to 65 percent.

How does apartment NOI affect property value?

Property value is calculated by dividing NOI by the market cap rate. A higher NOI at a fixed cap rate produces a proportionally higher valuation, which is why even modest NOI improvements translate into significant equity gains.

What DSCR do lenders require based on apartment NOI?

Most commercial lenders require a DSCR of 1.20 to 1.25, meaning NOI must exceed annual debt service by at least 20 to 25 percent. Properties that fall below this threshold typically cannot qualify for standard agency or bank financing without additional equity.

Recommended

Ready for a Luxer One® package locker quote?

Tell us your unit count and we'll send right-sized pricing with a fast response time.

Get my free quote